Required information

Wayland Custom Woodworking is a firm that manufactures custom cabinets and woodwork for business and residential customers. Students will have the opportunity to establish payroll records and to complete a month of payroll information for Wayland. Wayland Custom Woodworking is located at 1716 Nichol Street, Logan, Utah, 84321, phone number 435-555-9877. The owner is Mark Wayland. Wayland’s EIN is 91-7444533, and the Utah Employer Account Number is 999-9290-1. Wayland has determined it will pay their employees on a semimonthly basis. Federal income tax should be computed using the percentage method.

For Part 1 of this project, you will complete payroll for the entire fourth quarter (Q4) of 2016, which consists of the final six pay periods of the year. Once payroll has been completed for the fourth quarter, you will then file the annual tax forms for Wayland as well as prepare each employee’s Form W-2 in Part 2.

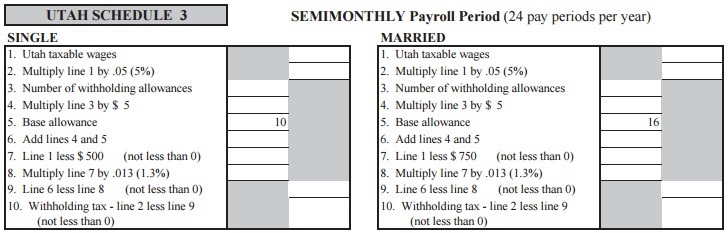

The SUTA (UI) rate for Wayland Custom Woodworking is 2.6% on the first $32,200. The state withholding rate is 5.0% for all income levels and marital statuses, which will be used in computing Utah withholding tax for each employee using the tax tables provided below.

Rounding can create a challenge. For this project, the hourly rate for the individuals should be rounded to five decimal places. So take their salary and divide by 2,080 (52 weeks at 40 hours per week) for all full time employees, both exempt and nonexempt. For nonexempt employees, such as StevonVarden, Varden’s salary is $42,000 and is a nonexempt employee, so the calculation will be $42,000/2,080, which would give you $20.19231 per hour, and use this to compute the employee’s gross pay based on the number of hours worked. When a nonexempt employee has worked overtime hours for a given pay period, take their regular hourly rate and multiply it by 1.5, round the result to 5 decimal places, and multiply the new rate by their number of overtime hours.

For exempt employees, such as Anthony Chinson, an hourly rate rounded to five decimal places should be determined using the same method shown above, but gross pay should be determined by taking the exempt employee’s yearly salary and dividing it by 24, which is the number of payroll periods with a semimonthly frequency. For example, Chinson’s salary is $24,000 and is a full time employee. Chinson’s hourly rate is $11.53846 (determined by taking $24,000/2,080), but as he is an exempt employee, the calculation for his gross pay will be $24,000/24, which would give you $1,000. For pay periods that include paid holidays, ensure to distribute an exempt employee’s regular pay accordingly to holiday pay based on the number of hours that consist of the holidays for that period.

Employees are paid for the following holidays occurring during the final quarter:

- Thanksgiving day and the day after, Thursday and Friday November 24-25

- Christmas, which is a Sunday. When holidays occur on a weekend, the preceding Friday, December 23, is considered a holiday. Employees receive holiday pay for Monday, December 26.

For the completion of this project, refer to the tax-related information in the table below. For federal withholding calculations, use the percentage method tables in Appendix C, which is provided below. For Utah state withholding calculations, use the Utah Schedule 3 tax tables linked below (ensure to use the appropriate Utah table based on each employee’s marital status). Both 401(k) and insurance are pretax for federal income tax and Utah income tax.

| Federal Withholding Allowance (less 401(k), Section 125) | $168.80 per allowance claimed |

| Semimonthly Federal Percentage Method Tax Table | Appendix C Page 254 Table #3 |

| Federal Unemployment Rate (employer only) (less Section 125) | 0.6% on the first $7,000 of wages |

| State Withholding Rate (less 401(k), Section 125) | See Utah Schedule 3, Table 1 or use the Excel Version of Schedule 3 |

| State Unemployment Rate (employer only) (less Section 125) | 2.6% on the first $32,200 of wages |

{kind=link}

The balance sheet for WCW as of September 30, 2016, is as follows:

| Wayland Custom Woodworking Balance Sheet 9/30/2016 | ||||||

| Assets | Liabilities & Equity | |||||

| Cash | $ | 1,125,000.00 | Accounts Payable | $ | 112,490.00 | |

| Supplies | 27,240.00 | Salaries and Wages Payable | ||||

| Office Equipment | 87,250.00 | Federal Unemployment Tax Payable | ||||

| Inventory | 123,000.00 | Social Security Tax Payable | ||||

| Vehicle | 25,000.00 | Medicare Tax Payable | ||||

| Accumulated Depreciation, Vehicle | State Unemployment Tax Payable | |||||

| Building | 164,000.00 | Employee Federal Income Tax Payable | ||||

| Accumulated Depreciation, Building | Employee State Income Tax Payable | |||||

| Land | 35,750.00 | 401(k) Contributions Payable | ||||

| Total Assets | 1,587,240.00 | Employee Medical Premiums Payable | ||||

| Notes Payable | 224,750.00 | |||||

| Utilities Payable | ||||||

| Total Liabilities | 337,240.00 | |||||

| Owners’ Equity | 1,250,000.00 | |||||

| Retained Earnings | – | |||||

| Total Equity | 1,250,000.00 | |||||

| Total Liabilities and Equity | 1,587,240.00 | |||||

October 1:

Wayland Custom Woodworking (WCW) pays its employees according to their job classification. The following employees comprise Wayland’s staff:

| Employee Number | Name and Address | Payroll information |

| 00-Chins | Anthony Chinson | Married, 1 Withholding allowance |

| 530 Sylvann Avenue | Exempt | |

| Logan, UT 84321 | $24,000/year + commission | |

| 435-555-1212 | Start Date: 10/1/2016 | |

| Job title: Account Executive | SSN: 511-22-3333 | |

| 00-Wayla | Mark Wayland | Married, 5 withholding allowances |

| 1570 Lovett Street | Exempt | |

| Logan, UT 84321 | $75,000/year | |

| 435-555-1110 | Start Date: 10/1/2016 | |

| Job title: President/Owner | SSN: 505-33-1775 | |

| 01-Peppi | Sylvia Peppinico | Married, 7 withholding allowances |

| 291 Antioch Road | Exempt | |

| Logan, UT 84321 | $43,500/year | |

| 435-555-2244 | Start Date: 10/1/2016 | |

| Job title: Craftsman | SSN: 047-55-9951 | |

| 01-Varde | StevonVarden | Married, 2 withholding allowances |

| 333 Justin Drive | Nonexempt | |

| Logan, UT 84321 | $42,000/year | |

| 435-555-9981 | Start Date: 10/1/2016 | |

| Job title: Craftsman | SSN: 022-66-1131 | |

| 02-Hisso | Leonard Hissop | Single, 4 withholding allowances |

| 531 5th Street | Nonexempt | |

| Logan, UT 84321 | $49,500/year | |

| 435-555-5858 | Start Date: 10/1/2016 | |

| Job title: Purchasing/Shipping | SSN: 311-22-6698 | |

| 00-Succe | Student F Success | Single, 1 withholding allowance |

| 1650 South Street | Nonexempt | |

| Logan, UT 84321 | $36,000/year | |

| 435-556-1211 | Start Date: 10/1/2016 | |

| Job title: Accounting Clerk | SSN: 555-55-5555 | |

Voluntary deductions for each employee are as follows:

| Name | Deduction |

| Chinson | Insurance: $50/paycheck |

| 401(k): 3% of gross pay | |

| Wayland | Insurance: $75/paycheck |

| 401(k): 6% of gross pay | |

| Peppinico | Insurance: $75/paycheck |

| 401(k): $50 per paycheck | |

| Varden | Insurance: $50/paycheck |

| 401(k): 4% of gross pay | |

| Hissop | Insurance: $75/paycheck |

| 401(k): 3% of gross pay | |

| Student | Insurance: $50/paycheck |

| 401(k): 3% of gross pay | |

The departments are as follows:

Department 00: Sales and Administration

Department 01: Factory workers

Department 02: Delivery and Customer service

You have been hired as of October 1 as the new accounting clerk. Your employee number is 00-SUCCE. Your name is Student F Success. Your address is 1650 South Street, Logan, UT 84321. Your phone number is 435-556-1211, you were born July 16, 1985, your Utah driver’s license number is 887743 expiring in 7/16/2018, and your Social Security number is 555-55-5555. You are considered a nonexempt employee, have one withholding allowance, and paid a rate of $36,000 per year.

Required:

- Complete the payroll process for Wayland Custom Woodworking’s fourth quarter pay periods. Please note that for pay periods after October 15, you mustcarry the current ending year to date (YTD) amounts as they appear from the prior pay period from each employee’s Employee Earning Records form (EERF) to the rows titled “Prior Period YTD”. Amounts from the current pay period will be auto-populated to the employee EERFs once you complete the payroll register, and will be combined with the prior period YTD amounts to determine the new current ending YTD amounts.

For example, if the year to date gross pay for Anthony Chinsonis $5,000 after the October 31 pay period, you would take this amount and add it to the appropriate input box for gross pay on the “Prior Period YTD” row for their November 15 EERF.

Additionally, you must carry the ending balance from each account in the prior period General Ledger to the following period’s General Ledger to the input boxes titled “Ending account balance from the prior period” before posting the payroll journal entries from the current period to the Ledger.

For additional instructions on how to carry information from one pay period to another, along with a guided walkthrough example of this process, refer to the project user guide in the project information section above.

October 15

October 15 is the end of the first pay period for the month of October. Employee pay will be disbursed on October 20, 2016. Any time worked in excess of 80 hours during this pay period is considered overtime for nonexempt employees. Remember that the employees are paid on a semimonthly basis.

- Complete the Employee Gross Pay tab.

- Complete the Payroll Register for October 15.

- Refer to the Employee Earning Record Forms for each employee for the current YTD amounts after you have completed the October 15 Payroll Register. Amounts from the current period are auto-populated from the Payroll Register.

- Complete the General Journal entries for the October 15 payroll.

- Post the journal entries to the General Ledger.

Part 1

October 31 is the end of the final pay period for the month. Employee pay will be disbursed on November 4, 2016. Any hours exceeding 88 during this pay period are considered overtime for nonexempt employees. Compute the employee pay below. Update the Employees’ Earning Records for the period’s pay and update the YTD amount. Remember that the employees are paid semi-monthly.

Part 2

Part 3November 15

Compute the pay for each employee. Update the Employee Earning record for the period’s pay and the new YTD amount. Employee pay will be disbursed on November 18, 2016. Any hours exceeding 88 during this pay period are considered overtime for nonexempt employees. Remember that the employees are paid semimonthly.

Part 4 November 30

Compute the Net Pay for each employee. Employee pay will be disbursed on December 5, 2016. Update the Employees’ Earning Record with the November 30 pay and the new YTD amount.

The company is closed and pays for the Friday following Thanksgiving. The employees will receive holiday pay for Thanksgiving and the Friday following. All the hours over 88 are eligible for overtime for nonexempt employees as they were worked during the non-holiday week.

Part 4 December 15

Compute the net pay and update the Employees’ Earning Record with the December 15 pay and the new YTD information. Any hours worked in excess of 80 hours during this pay period are considered overtime for nonexempt employees.

Part 6 December 31

The final pay period of the year will not be paid to employees until January 3, 2017. The company will accrue the wages for the final pay period only. Since the pay period is complete, there will not be a reversing entry for the accrual. As a result, paychecks will not be issued for this pay period since they will be paid in the following year and reflected on the Employee Earning Record forms for each employee when paid.

The company pays for the day before and the day of Christmas, and if the holiday is on a weekend, the company pays for the Friday before. Christmas fell on a Sunday, so employees will be paid for both the Friday and Monday as holiday pay. Employees worked extra hours on Saturday during the week of 12/23-12/29. Reminder, holidays and vacations are not included as hours worked for calculation of overtime.